[email protected]

Nous vous répondrons dans les 24 heures

La Poste Autrichienne 5.99 €

Coursier DPD 6.49 €

Service de messagerie GLS 4.49 €

Contact

Contact Comment faire ses achats

Comment faire ses achats

Assistance

Livraison

La Poste Autrichienne 5.99 €

Coursier DPD 6.49 €

Service de messagerie GLS 4.49 €

Guide d'achat

Nous sommes à votre disposition !

[email protected]

Mon compte

Accédez à une communauté d'amateurs de livres à travers le monde et bénéficiez d’une panoplie d'avantages.

Créer un compte gratuitement

▸

Vide :-(

0

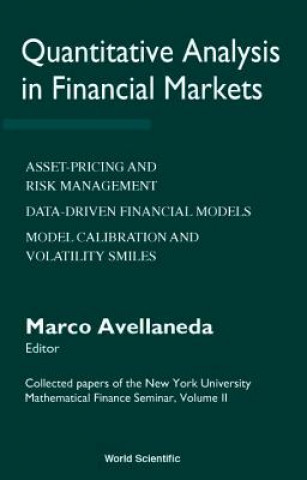

Quantitative Analysis In Financial Markets: Collected Papers Of The New York University Mathematical Finance Seminar (Vol Ii)

Langue

Anglais

Anglais

Anglais

Livre

Livre de poche

This volume contains lectures delivered at the celebrated Seminar in Mathematical Finance at the Cou...

Description détaillée

Code Libristo: 05066532

?

256 b

256 b

256 b

108.10

€

včetně DPH

50% de chance

Nous cherchons dans le monde

Quand vais-je recevoir mon livre ?

common.delivery_to

common.delivery_to

common.delivery_to

Politique de retour sous 30 jours

Ceci pourrait également vous intéresser

/

DVD

/

DVD

9.62

€

9.62

€

This volume contains lectures delivered at the celebrated Seminar in Mathematical Finance at the Courant Institute. The lecturers and presenters of papers are prominent researchers and practitioners in the field of quantitative financial modelling. Most are faculty members at leading universities or Wall Street practitioners. The lectures deal with the emerging science of pricing and hedging derivative securities and, more generally, managing financial risk. Specific articles concern topics such as option theory, dynamic hedging, interest-rate modelling, portfolio theory, price forecasting using statistical methods, and more.

À propos du livre

Nom complet

Quantitative Analysis In Financial Markets: Collected Papers Of The New York University Mathematical Finance Seminar (Vol Ii)

Langue

Anglais

Anglais

Reliure

Livre - Livre de poche

Date de parution

2001

Nombre de pages

380

EAN

9789810242268

ISBN

9810242263

Code Libristo

05066532

Poids

630

Dimensions

167 x 245 x 21