[email protected]

Nous vous répondrons dans les 24 heures

La Poste Autrichienne 5.99 €

Coursier DPD 6.49 €

Service de messagerie GLS 4.49 €

Contact

Contact Comment faire ses achats

Comment faire ses achats

Assistance

Livraison

La Poste Autrichienne 5.99 €

Coursier DPD 6.49 €

Service de messagerie GLS 4.49 €

Guide d'achat

Nous sommes à votre disposition !

[email protected]

Mon compte

Accédez à une communauté d'amateurs de livres à travers le monde et bénéficiez d’une panoplie d'avantages.

Créer un compte gratuitement

▸

Vide :-(

0

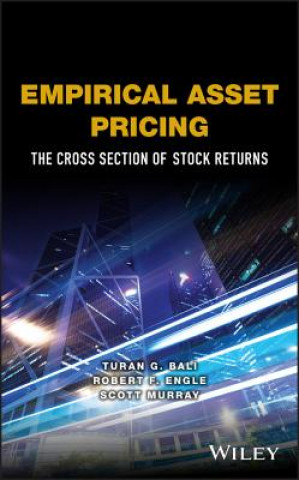

Empirical Asset Pricing - The Cross Section of Stock Returns

Langue

Anglais

Anglais

Anglais

Livre

Livre relié

Written by two experts in the field (including a renowned Nobel Prize Laureate), this book represent...

Description détaillée

Code Libristo: 09531701

?

334 b

334 b

334 b

141.39

€

včetně DPH

Stockage externe en petites quantités

Expédition sous 4-7 jours

common.delivery_to

common.delivery_to

common.delivery_to

Politique de retour sous 30 jours

Ceci pourrait également vous intéresser

/

Livre de poche

/

Livre de poche

13.80

€

13.80

€

Written by two experts in the field (including a renowned Nobel Prize Laureate), this book represents an up-to-date compilation of empirical asset pricing theory and their techniques and application keeping emphasis throughout on empirical research and findings. Covering topics such as the mean-variance portfolio theory, the capital asset pricing model, and the arbitrage pricing theory, this is an ideal text for courses on asset pricing as well as on portfolio/risk management/finance, stocks and bonds, and arbitrage

À propos du livre

Nom complet

Empirical Asset Pricing - The Cross Section of Stock Returns

Auteur

Turan G. Bali, Robert F. Engle, Scott Murray

Langue

Anglais

Anglais

Reliure

Livre - Livre relié

Date de parution

2016

Nombre de pages

512

EAN

9781118095041

ISBN

1118095049

Code Libristo

09531701

Éditeurs

John Wiley & Sons Inc

Poids

1150

Dimensions

243 x 166 x 31